May 7, 2026

By Matthew Bolig

Senior Advisor, Product & Technology Marketing

As AI infrastructure scales, the limitations of pluggable optics in the data center are becoming increasingly apparent. Ciena’s Matt Bolig explains how this shift is setting the stage for co-packaged optics to redefine how bandwidth is delivered inside the data center.

There is an inflection point approaching in data center networking with a new technology that is forecasted to supersede pluggable optical modules for highest port count shipments. To be sure, the pluggable optics market will continue to grow for some time, however, the trend towards a more efficient interconnect technology is clear.

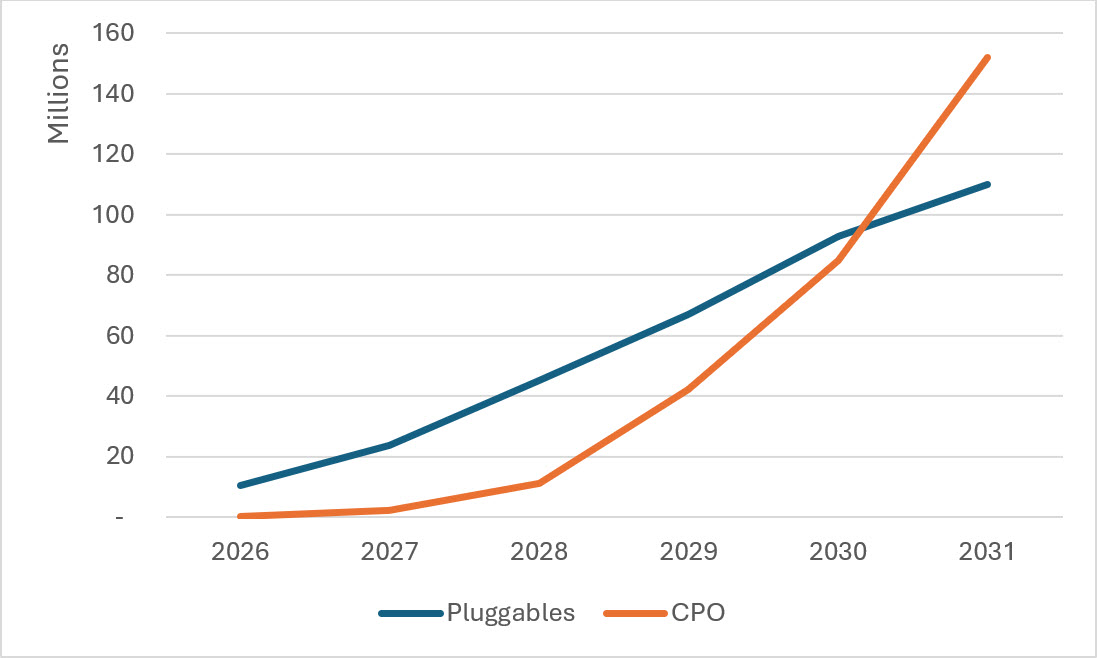

The technology forecasted to surpass pluggables is, of course, co-packaged optics (CPO). The dawn of this new networking age - the Age of CPO - can clearly be seen in the chart below based on data from research firm LightCounting that shows, for advanced data rates of 200Gbps and beyond, CPO is expected to overtake pluggables by around 2031.

Source: LightCounting Ethernet Optics Forecast March 2026

Figure 1. Optical port count forecast for 224Gbps+ links up to 2km

Beneath “AI’s insatiable demand for bandwidth” are several important forces driving this paradigm shift. Understanding these dynamics will be critical in the coming years, as the forecasted transition will be pulled and pushed by both underlying technology and business currents.

To provide context for our current market conditions, it’s helpful to start this exploration with a look back. For the past two decades, standardized pluggable optics have been the workhorse of intra-data center networks all over the world, delivering economical, reliable links up to 2km. While the vision of standardized, disaggregated optics was always clear, there were many fits and starts along the way, and there were certainly points in the early 2000’s where the path seemed murky, to say the least. Anyone who worked on XENPAK modules that required a PCB cutout is keenly aware of how wobbly things were at the beginning of the pluggable era.

However, two decades of focused work by standards committees such as IEEE and OIF, along with the incredible efforts of transceiver providers, have led to one of the great supply chain stories in technology today. Annual volumes for leading-edge optical modules are now measured in 10’s of millions of units per year.

Given the size of this base, it is reasonable to assume that pluggables would have sufficient inertia to retain optical form factor dominance for the foreseeable future. However, notable friction is now appearing in the system with the rapidly evolving requirements of AI factories straining the front panel pluggable architecture along multiple vectors.

Plugs running out of steam

Over the last few years, it has become apparent that technologies that were acceptable for the initial cloud networking era are no longer sufficient for the age of AI. Such is the case with pluggable optics.

A prime example is routing density. Just three years ago, this was a non-issue as rack densities were limited by cooling capabilities. This changed as AI drove the widespread adoption of liquid cooling, which now moves the constraint on how many chips can be accommodated in a switch or compute tray to how much bandwidth can be networked out of the tray – across just two available data escape surfaces: The box’s front panel and its back panel, and these have to be shared with power and cooling as well.

Another significant issue with retimed, pluggable optics is the cost of implementing electrical connectivity to the front panel. These costs manifest in two forms: watts and dollars. Both of these costs increase with each network generation due to the DSPs used within modules to preserve signal integrity. There have been recent efforts to reduce these costs by eliminating either the retimer receive path (Retimed Transmit Linear Receive configuration) or the retimer entirely (Linear Pluggable Optics configuration), however these technologies have, to date, not proven attractive enough to gain widespread adoption for various cost and performance reasons. Concurrently, there has been significant effort put into reducing DSP retimer power consumption (pJ/bit) and cost ($/bit), but the exploding number of bits driven by AI is still pushing retimer cost multipliers to unsustainable levels.

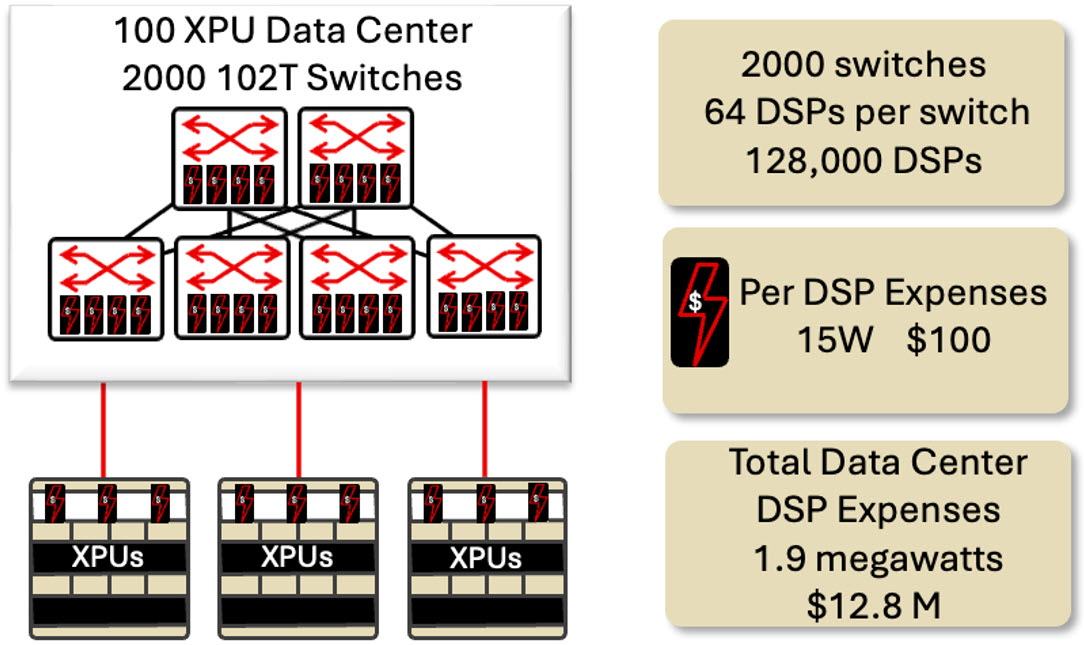

Figure 2. Cost of DSPs in AI data center

Consider a 102 Tbps switch box with 64 x 1.6 Tbps optical modules as shown in Figure 2. Each 1.6T, 3nm DSP is estimated to consume about 15W. This means that the power for just the DSPs is about 1kW – in the same range as the switch chip itself. Volume pricing for 1.6T DSPs is forecasted to be on the order of $75 per unit. However, this gets margined up by ~30% by transceiver builders, so the total cost to the end user is on the order of $6,000. For a 100k XPU data center with 2k switches, the total DSP cost is in the neighborhood of 2 megawatts and $13M.

Co-packaged optics progress

CPO has been around for quite some time and has always offered higher density than pluggable optics, as well as a path to eliminate retimer costs. Why, then, is CPO only starting to gain acceptance now?

Certainly, the work done by Broadcom and NVIDIA is an important factor. Broadcom has continued to invest in CPO technology over the past several years, culminating in reliability testing currently being conducted with Meta, which most recently showed 36 million hours of operation with no catastrophic system failures, as highlighted in this summary. NVIDIA, for its part, is taking on first-mover risk with initial deployments of Quantum-X and Spectrum-X CPO switches this year.

While the innovation has been remarkable, some would argue that these developments are only a first step. The concern is that these initial CPO implementations are effectively "walled gardens". For end-users, this kind of approach can result in vendor lock-in and limited buyer power. These dynamics are broadly seen as undesirable as they run counter to the competitive, robust supply chains customers have come to expect from pluggable optics.

Open CPX MSA

Recent progress has been made to provide a framework for CPO technology that delivers the reduced cost and power benefits of CPO in a structure that also preserves the flexibility and supply chain benefits of pluggables. This progress has come in the form of the Open CPX Multi-Service Agreement (MSA), which was announced on March 12th 2026.

Figure 3. Open CPX MSA member companies

The goal of the organization is to standardize a pluggable form factor that can be used for both co-packaged and near package optics. The first revision of the MSA is focused on optical connectivity with copper connectivity being added later, enabling end-users to develop a single PCB that works for both technologies. Each module supports 32 bi-directional channels for a total of 6.4Tbps total throughput per module, utilizing 200Gbps lane speeds. The Open CPX MSA also features a strong roadmap with clear line of sight to both 12.8Tbps modules and to 448Gbps per lane support.

Figure 4. CPX interconnect

The vision of Open CPX is to provide an open infrastructure akin to the tremendously successful front-panel ecosystem that has fueled data center growth over the past quarter of a century, ensuring a robust, cost-competitive supply chain that can deliver at the massive volumes required for future AI factories where demand is expected to skyrocket as optics moves into scale up networks. This is the true strength of the MSA.

The CPX connector has multiple sources ensuring a robust connector supply chain. This means that some of largest connector companies in the world can bring their collective might to deliver both CPX connectors and associated CPC at scale.

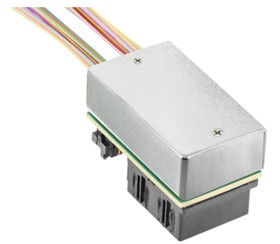

At OFC 2026, Ciena, Terahop and Coherent all showed off 6.4Tbps connector based optical engines - including Ciena’s Vesta 200 6.4T CPX. Each company brings significant optical design and manufacturing expertise and infrastructure to deliver this critical technology at the scale required by the industry.

Figure 5. Vesta 200 6.4T CPX pluggable CPO module

The path to an open CPO ecosystem

We are at the brink of a new age of optical connectivity as CPO emerges as the next significant data center networking technology. Momentum behind CPO is beginning to build, thanks to the efforts of extremely large networking equipment providers. For CPO technology to achieve broad adoption, however, an open ecosystem approach is called for, as we have with pluggable optics today. The Open CPX MSA provides a foundational framework for this open approach.